Airbnb Business Model & Revenue Strategy: 5 Insights for New-Age Businesses

6714 Views 2 min January 8, 2026

Sameer is a skilled technical content writer with over 8+ years of experience in the industry. He has a strong grasp of topics like AI, software development, IT solutions, and hardware technologies. Sameer is currently part of Apptunix, an enterprise mobile app development company that helps businesses build innovative digital products and solutions. At Apptunix, he focuses on crafting engaging content that makes complex ideas easy to understand. His work helps tech companies connect with their audience and communicate real value.

The banking sector has undergone a profound transformation that has reshaped its very foundations. Who could have imagined a time when individuals could manage their finances entirely through smartphone apps like N26? However, this seemingly strange concept has now become the new normal.

This transformation can be likened to a revolution, and at the forefront of this revolution is the innovative entity known as Neo Bank.

Neo banks have emerged as a disruptive force in the banking ecosystem, customers no longer need to deal with cumbersome paperwork. Instead, you can have financial services at your fingertips.

As a result, the global neobanking market reached a substantial value of USD 148.93 billion in 2024. The projections indicate a remarkable compound annual growth rate (CAGR) of 40.29% from 2025 to 2034.

Also read: Cost for Neobank app development like Sofi

The onset of the COVID-19 pandemic further fueled this growth, as people increasingly relied on online banking services. Notably, in 2020, Indian neobank startups secured over USD 200 million in funding, exemplifying the sector’s rapid ascent.

If you’re inspired by the remarkable success stories of neobanks like N26, Monzo, or Revolut, then this blog is an invaluable guide for you. Through a comprehensive analysis, we aim to uncover the secrets behind N26’s business model, to help you develop your platform based on these learnings.

So, let’s begin!

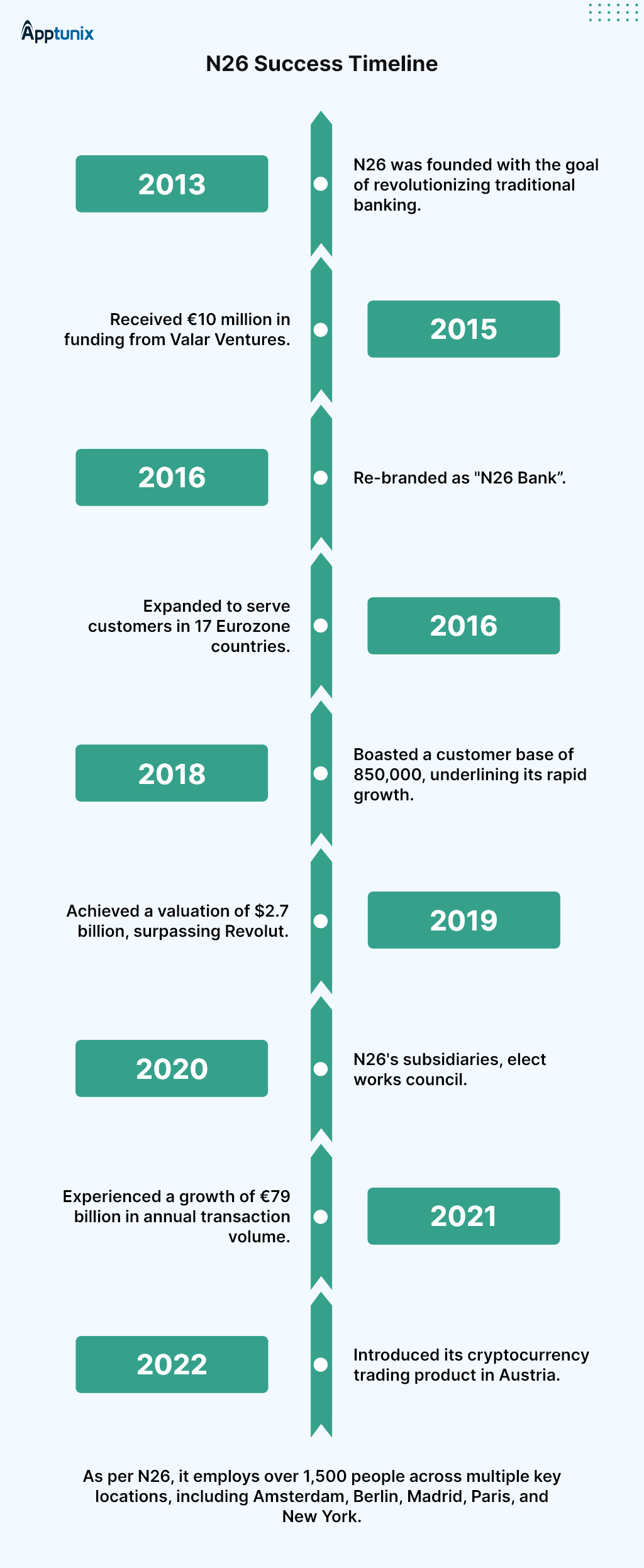

In 2013, Valentin Stalf and Maximilian Tayenthal founded N26 as a fintech startup, initially named “Number 26.” The goal was to provide prepaid cards for teenagers, controlled by parents. By 2014, the team realized the need to pivot. The real-time connection between the card and the app was a hit, signaling an opportunity to challenge traditional banks.

Despite facing numerous challenges and initial skepticism, the N26 team accomplished a remarkable feat by securing a banking license in Germany within a mere year of its founding. This achievement, which many deemed nearly impossible gave a new vision. The company rebranded as “N26” in July 2016, a remarkable moment in its evolution as it embarked on a journey to redefine the future of banking through digital innovation.

1.Rapid Expansion and Valuation (2017-2019)N26 expanded its digital banking mobile app development services across Europe, amassing a growing customer base. In January 2019, it raised $300 million in a funding round, achieving a valuation of $2.7 billion, surpassing competitors to become Europe’s most valuable mobile bank.

2.U.S. Entry and Further Funding (2019-2020)The U.S. market beckoned, and N26 made its soft launch in July 2019, partnering with Axos Bank. Additional funding rounds followed, extending its funding and valuing the company at $3.5 billion. However, in February 2020, N26 announced its withdrawal from the UK due to Brexit-related regulatory changes.

3.Internal Developments (2020-2022)N26 continued to evolve internally. Subsidiaries elected works councils in late 2020. In 2021, experienced executive Jan Kemper joined as CFO, later taking on the role of COO. In October 2021, N26 secured a significant $900 million in a funding round, reaching an impressive valuation of $9 billion.

4.Exit from the U.S. and Legal Changes (2021-2022)In November 2021, N26 announced its exit from the U.S. market, opting to concentrate on its European core business. In a major move in November 2022, N26 changed its legal structure from a German Limited Liability Company (GmbH) to a German Stock Corporation (AG). A new five-member board of directors was appointed, signaling further changes on the horizon.

5.Rising from the Ashes of Past ChallengesN26 continues to captivate with its dynamic expansion strategies. In a move that showcases its relentless global ambition, N26 unveiled its presence in Brazil in May 2023. This momentous launch follows the company’s earlier announcement of its entry into the Latin American market in 2019. N26’s ability to navigate complexities and overcome setbacks helps it consistently push the boundaries of digital banking. This also demonstrates its unwavering commitment to providing innovative financial solutions on a global scale.

Being a financial solutions provider, N26 operates as a platform that seamlessly integrates various elements into its business model.

To better understand its approach, let’s delve into the N26 business model canvas.

Now that you understand that N26’s business model reflects a holistic approach to delivering an efficient digital banking experience. Going ahead, let’s explore how N26 makes money.

Bonus Read: How Much Does It Cost to Build an App Like N26

While N26 is seen as a big challenge, the way it earns money is quite similar to traditional banks. In 2021, N26 went beyond its basic banking and payment systems, adding new services to generate revenue. This broadened their sources of income in the sector.

Now, let’s break down how N26 makes money.

1.Subscription RevenueN26 earns its primary income from various subscription plans for both individuals and business users. There are four main plans:

2.Insurance CommissionN26 collaborated with insurance robo-advisor Clark. to provide various insurance plans, covering areas like liability, legal, household, automotive, health, disability, and more.

Users who haven’t subscribed to N26 Metal can opt for these insurance plans separately. N26 earns a minimum of €4.76 per insured product. In the insurance realm, N26 acts as an intermediary, connecting users with traditional insurance brokers.

3.Interest On Cash DepositN26 follows a conventional banking practice of utilizing user account deposits by lending them to other financial institutions, earning interest known as Net Interest Margin (NIM).

A portion of this interest is shared with users as savings account interest. N26 offers up to 1.38% interest on cash held in its savings accounts, aligning with standard banking practices.

4.Loan InterestN26’s revenue stream includes loan interest. The company provides personal loans ranging from €1,000 to €50,000 through its N26 Credit division, with repayment periods spanning 6 to 48 months. N26 profits by applying interest rates on these loans, ranging from 1.99% to 19% per year.

Also, N26 has partnered with auxmoney, Germany’s leading loan marketplace. This expands loan options for users and increases their income from interest charges.

5.Buy Now Pay LaterN26 participates in the popular “Buy Now Pay Later” trend, a concept favored by many fintech companies. Users can split expenses up to €500 into 3-6 month installments. N26 generates revenue from this service by imposing an annual interest rate, which ranges from 7.49% to 11.99%, determined by the user’s credit score.

Also Read: An Ultimate Guide to Developing Mobile Apps for Foldable Devices

1.N26 partners had flexibility in their visionN26 didn’t start as a digital bank. Initially, they aimed to provide prepaid cards for teenagers, managed by parents. But when they noticed parents were using it for themselves. They swiftly adapted to the idea of becoming a digital bank, focusing on user-friendly mobile banking.

2.N26 addressed the problem customers hadN26 understood the importance of solving real customer issues. Instead of assuming what customers needed, they identified common frustrations and inconveniences people faced with traditional banks. This customer-centric approach guided their development.

Also read: Blockchain in Banking

3.Focusing on creating value, not a buzz!N26’s success wasn’t built on flashy gimmicks but on creating genuine value. They leveraged the technology intending to simplify banking. They also offered a more cost-effective, flexible, and user-friendly alternative to traditional banks. This focus on real value helped them acquire customers efficiently without excessive advertising.

N26’s journey is an inspiring one that has appreciably impacted the fintech industry, transforming the way people bank. We have covered all the significant aspects from how N26 works, and its revenue model, to its business canvas for your understanding. So that you can embark on such a venture effortlessly.

For those interested in building similar apps like N26, Apptunix offers valuable expertise and assistance. We provide a wide range of services to empower your development journey.

Apptunix is a trusted app development company where vision becomes a digital reality.

Q 1.What is N26's business model?

N26 operates as a fully digital bank with no physical branches. Its business model focuses on convenience, transparency, and innovation. Unlike traditional banks, it provides a mobile-first banking experience, allowing users to manage finances from their smartphones.

Q 2.How does N26 make money without charging fees?

Even though N26 offers free banking services, it has multiple revenue streams. It earns from premium accounts (N26 Smart, You, and Metal), interchange fees when customers use their cards, and partner services like travel insurance and investment products.

Q 3.What services does N26 offer?

N26 provides various digital banking services, including a free bank account, instant payments, real-time transaction alerts, and smart budgeting tools like Spaces (sub-accounts for saving goals). It supports contactless payments and offers cashback rewards on selected purchases. N26 also provides international money transfers, ATM withdrawals, and premium services.

Q 4.Why choose N26 over traditional banks?

N26 offers a modern, mobile-first banking experience that eliminates unnecessary fees and paperwork. It provides real-time notifications, smart budgeting tools, and an intuitive app that makes managing money easy. Unlike traditional banks, it has a transparent fee structure, no hidden costs, and faster transactions.

Get the weekly updates on the newest brand stories, business models and technology right in your inbox.

Sameer is a skilled technical content writer with over 8+ years of experience in the industry. He has a strong grasp of topics like AI, software development, IT solutions, and hardware technologies. Sameer is currently part of Apptunix, an enterprise mobile app development company that helps businesses build innovative digital products and solutions. At Apptunix, he focuses on crafting engaging content that makes complex ideas easy to understand. His work helps tech companies connect with their audience and communicate real value.

6714 Views 2 min January 8, 2026

717 Views 2 min December 26, 2025

750 Views 2 min December 23, 2025

Book your consultation with us.

Book your consultation with us.

One Central, The offices 3, Level 3, DWTC, Sheikh Zayed Road, Dubai

+971 50 782 1690