The Future of Mobile App Development: Predictions and Trends to Watch Out For

2191 Views 2 min May 12, 2023

Hardeep Singh is a seasoned B2B technical writer at Apptunix with a sharp eye for strategy and a mind wired for innovation. With over a decade of experience in technical and SEO writing, and a Master’s degree in Wireless Communication, he’s written across domains including AI, Blockchain, IoT, Cybersecurity, and beyond. At Apptunix, Hardeep drives content that bridges business goals with future-ready mobile and web solutions, thus helping startups and enterprises make smarter digital decisions.

Blockchain technology has taken the business world by storm. There is no second opinion that this technology is going to stay here for a long time. This is the reason why most businesses from around the globe want to implement blockchain into their business.

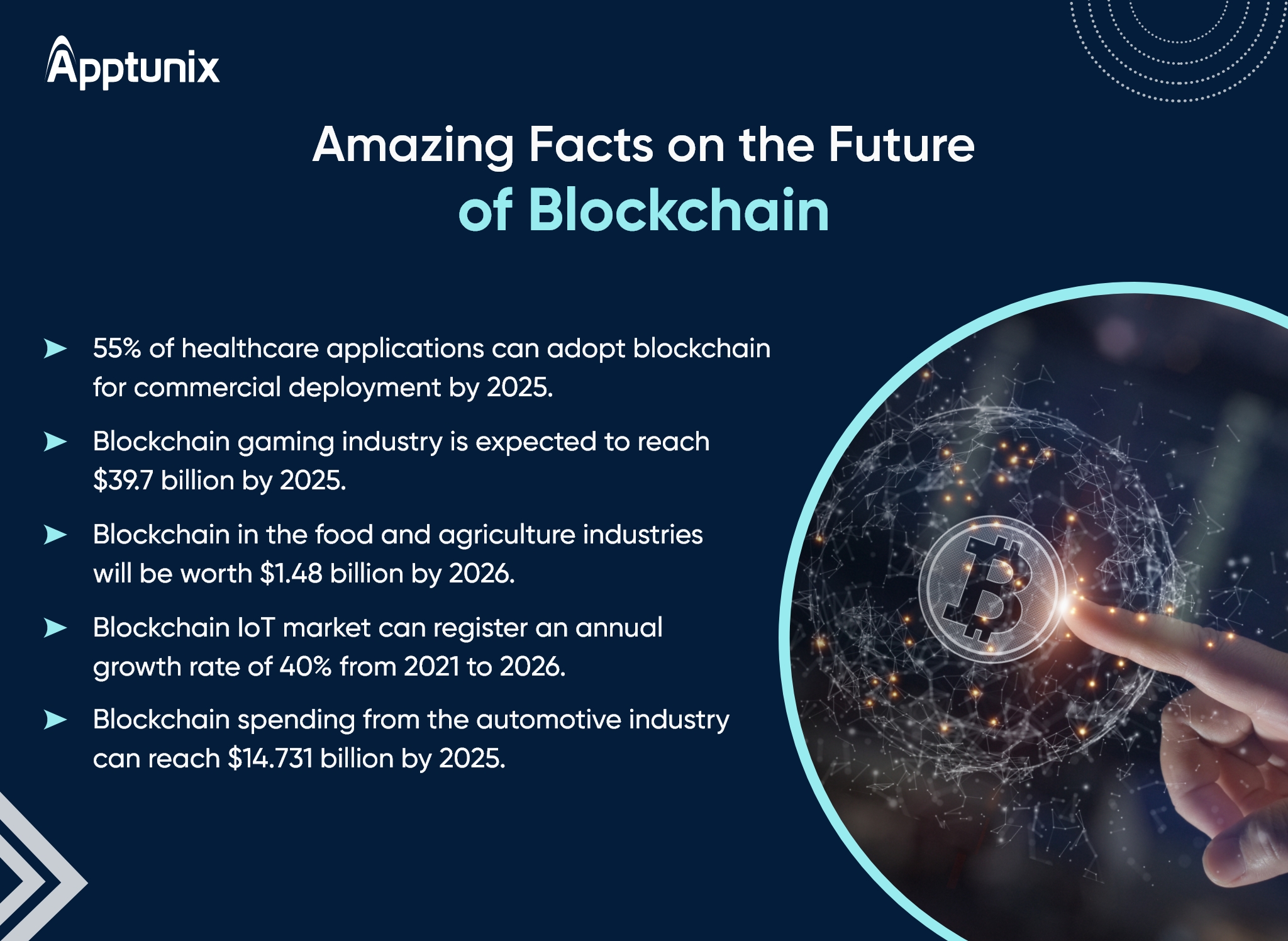

And why not so when this distributed encrypted database model has a high potential to solve online trust and security-related problems? Even the statistics speak on its behalf. According to a recent survey, the compound annual growth rate of 56.3% is going to make the blockchain industry worth $163.83 billion by 2029.

So if you are planning to set up blockchain in your business it’s the right time to dive in. But blockchain implementation is not as easy as it seems to be. To make it easy for you this guide offers everything you must know about integrating blockchain technology into your business.

So let’s begin the journey without any delay.

You might be wondering whether it’s a wise decision to go with blockchain or not. Well, blockchain technology has a lot to offer. It has become one of the key technologies to drive business transformation. Some of its major advantages are

Also Read: Top Decentralized Exchanges (DEX)

Also Read: How Is Blockchain Technology Revolutionizing Mobile Apps?

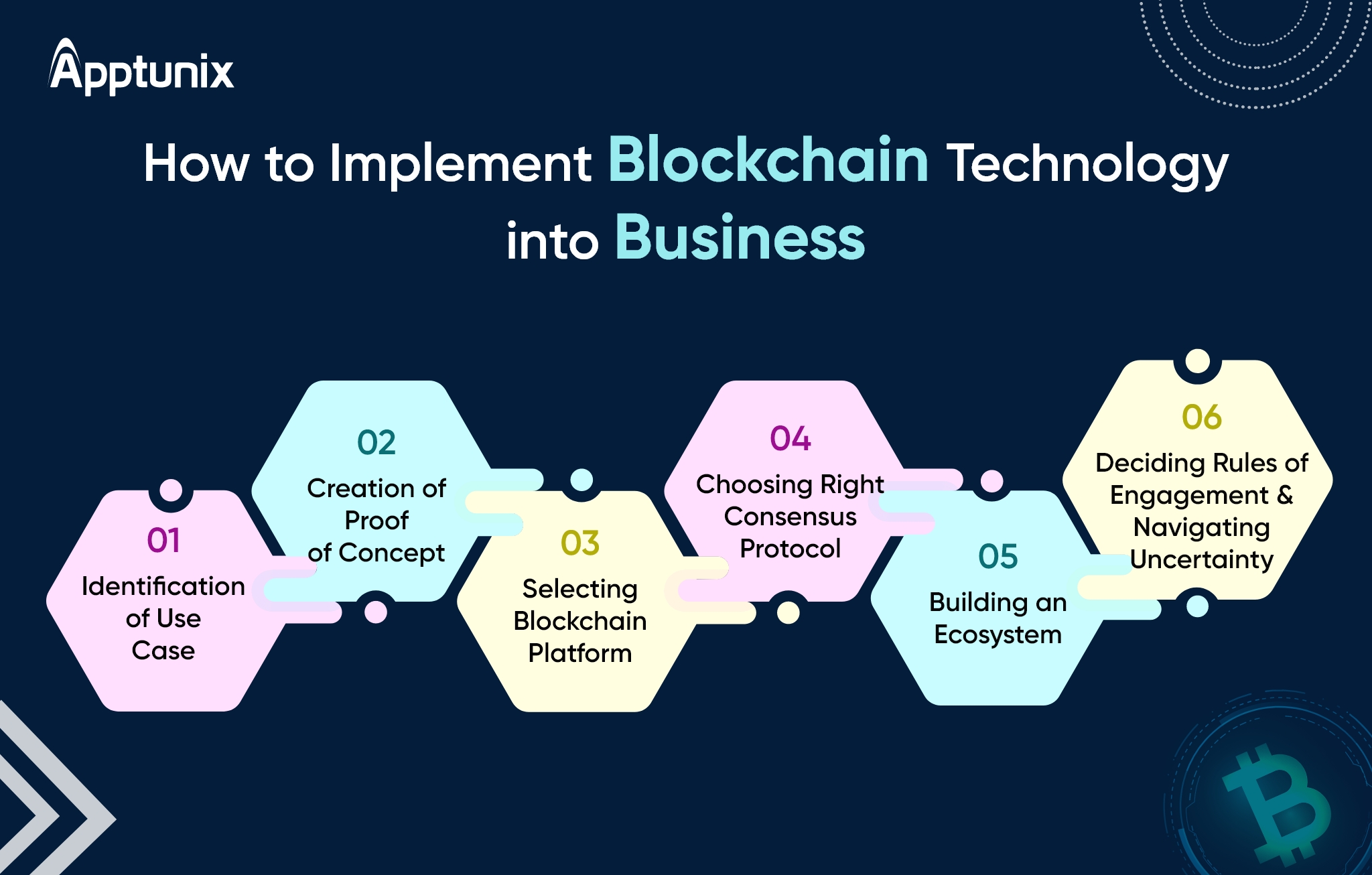

Blockchain implementation needs a complete strategy. You are required to consider both the current situation as well as the future plans before making a move. To make it easy, here is a complete step-by-step process to implement blockchain successfully.

It is essential to identify, clarify and organize your business needs. You must be clear about the problems in hand that you want to solve via blockchain. The best way is, to go with the pilot project, analyze the outcomings, and then proceed further. It is good to ask yourself questions like

Once the use case is identified, it is necessary to make a valid proof of concept (PoC). PoC is a strategic procedure used for the evaluation of blockchain feasibility for the business. All you need to do is to understand the planning phase and evaluate the steps. Let’s go through some steps to create a PoC.

It is crucial to carefully choose the blockchain platform. You must be aware of the technology that suits your business. It is good to ascertain whether the technical team is organized and equipped with an open-source station. Apart from this, budget, the general level of understanding, etc are some of the factors you can consider while choosing the platform. To help you with the same, here are some of the popular blockchain development platforms:

- Ethereum

It is basically used for building innovative contracts. A reason why it is being used by several organizations for determining the potential scaling rate. Ethereum is one of the best options for businesses that want to build apps capable of running on blockchain-like software.- Hyperledger Fabric

This platform is basically used for building creative private blockchain apps. A Hyperledger expert can develop technical solutions that build organizations through the implementation of blockchain in an app.- Stellar

This platform supports a distributed exchange mode that allows users to easily send payments in specific currencies. This is due to the fact that the network automatically performs the forex conversion.- Quorum

The good thing about Quorum is, it eliminates data tampering in business transactions. This allows organizations to make secure transactions while maintaining privacy.- Multichain

As indicated by its name itself this platform can be employed in various industries. It doesn’t matter whether it’s the healthcare sector, education sector, banking & finance sector, eCommerce sector, or so on Multichain is a good option to go with.- OpenChain

If you are looking forward to maximizing every aspect of your business’s Human Resource Management (HRM), OpenChain is one of the best options to go with.

Also Read: Top 5 Blockchain Development Platforms to Build Robust Applications

When it comes to a distributed network, consensus protocol alone is capable of creating an indisputable system of agreement between the devices. Some of these protocols are

Blockchain technology functions best with the participation of stakeholders. So you are required to build an industry ecosystem, a community within the organization that can understand the technology’s potential and helps to improve standards & rules.

Stakeholders can decide the rules, decide the right control framework, ensure costs & benefits, affirm governance mechanisms and validate various other blockchain functionalities. To make it easy for you, here are steps to build a solid ecosystem.

The new ecosystem must carry the ability to solve the organization’s issues. It must also address the privacy implications, compliances, and cybersecurity issues. Make sure that your business must comply with the emerging blockchain policies and best practices. Here is the key plan to help you out on the same.

Also Read: Best Blockchain Development Companies

Implementing blockchain technology into business has its own challenges. So you must be aware of certain things that must be considered while implementing this technology.

# Interesting Fact: 88% of senior executives worldwide think that blockchain technology is soon going to achieve mainstream adoption.

Needless to say, you are going to face a lot of challenges while implementing sophisticated blockchain technology into your business. Let’s have a look at some of the common challenges.

Whatever the challenges are, blockchain technology is helping businesses across the world set new records. Whether we talk about blockchain leaders, blockchain engineers, business owners, or entrepreneurs, all are showing high interest in integrating blockchain technology.

So if you want to be a part of the trending revolution it’s the right time to dive in. What you are required to do is to hire blockchain implementation experts that can help you make a mark in the global blockchain business community.

Q 1.Can I Build My Own Blockchain?

Yes, you can. You are free to write your own code for creating a new blockchain that is capable of supporting cryptocurrency. All it needs is extensive technical training for enhancing your coding skills and basic understanding of blockchain technology. You can also hire blockchain development company to do the job better.

Q 2.How Much Does It Cost to Build a Blockchain App?

On average, the blockchain app development cost typically ranges from $25,000 to $200,000. This cost can vary depending on the app’s complexity, the features you want, and several other factors. To get an estimated cost for your dream app you can book a free consultation.

Q 3.How Much Time Does It Take to Build a Blockchain App?

Well, for an average app, this period ranges between 3 to 6 months. It can change depending on the customization level and complexity of the app.

Q 4.Which is the Top Blockchain Platform?

Well, the list is large but Ethereum can be your choice. It is one of the oldest and most established decentralized networks. Moreover, it is less vulnerable to hacking, and power outages. There are also other options you can go with.

Get the weekly updates on the newest brand stories, business models and technology right in your inbox.

Hardeep Singh is a seasoned B2B technical writer at Apptunix with a sharp eye for strategy and a mind wired for innovation. With over a decade of experience in technical and SEO writing, and a Master’s degree in Wireless Communication, he’s written across domains including AI, Blockchain, IoT, Cybersecurity, and beyond. At Apptunix, Hardeep drives content that bridges business goals with future-ready mobile and web solutions, thus helping startups and enterprises make smarter digital decisions.

Book your consultation with us.

Book your consultation with us.

One Central, The offices 3, Level 3, DWTC, Sheikh Zayed Road, Dubai

+971 50 782 1690

Offer Ends Soon

Get a quick expert response in under 5 minutes.