10 Must-Have Features for a Fintech App That Users Actually Trust

111 Views 14 min June 25, 2026

Hardeep Singh is a seasoned B2B technical writer at Apptunix with a sharp eye for strategy and a mind wired for innovation. With over a decade of experience in technical and SEO writing, and a Master’s degree in Wireless Communication, he’s written across domains including AI, Blockchain, IoT, Cybersecurity, and beyond. At Apptunix, Hardeep drives content that bridges business goals with future-ready mobile and web solutions, thus helping startups and enterprises make smarter digital decisions.

Have you ever wondered why global businesses struggle to offer simple and trusted payment experiences in every country they enter?

Well, the answer lies in the way payments work across borders. Every region follows its own rules, habits, and local payment preferences. The shift toward digital commerce has widened this gap. Businesses now want payment systems that feel global yet adapt to local needs. This rising demand sets the direction for the next wave in FinTech.

Furthermore, if we look at recent statistics, digital payments are growing at an incredible pace. The global payments market is on track to jump from $788.06 billion in 2025 to $1,131.49 billion in 2029, showing a strong CAGR of 9.5 percent. This rise reflects the rapid shift toward online transactions by consumers and merchants. The shift also shows how much pressure businesses face to create payment experiences that work anywhere, for anyone.

One reason why glocal payment system development is emerging is that traditional global payment tools cannot meet local expectations anymore. Customers in India rely on UPI. Shoppers in Brazil trust Pix. Buyers in China use Alipay. Each region follows its own preferred rails. So, companies that want to scale globally must offer these local payment methods without losing global reach. This is where the glocal payment platform development approach becomes so powerful.

A glocal payment system combines global payment reach with the comfort of local acceptance. It supports multiple currencies and handles local payment methods that people trust in their own regions. It also adapts to local rules, languages, interfaces, and compliance needs. This balance helps businesses offer payment experiences that feel familiar to local users while operating on a global scale.

Global gateways follow broad international standards. Local payment service providers focus only on specific markets. A glocal payment system sits between the two. It merges worldwide coverage with regional customization. Businesses can leverage scale while meeting local expectations without building separate systems for every country.

In simple words, a glocal payment system blends the reach of global payments with the comfort of local acceptance. It allows a business to operate worldwide while supporting the payment habits, currencies, and regulations of individual markets. The idea feels simple at first, yet it solves one of the biggest challenges in cross-border commerce.

Several forces are pushing the world toward glocal payment adoption. Mobile payments continue to grow. Financial inclusion programs bring millions of new users online. Countries are testing or launching Central Bank Digital Currencies. Open banking rules allow safe sharing of financial data. Fraud prevention tools are improving. These changes create a perfect environment for glocal payment innovation.

IMF research highlights how interoperability drives faster adoption. Their findings show that payment systems scale better when local rails connect seamlessly across regions. The insights also show that nations that invest in real-time, interoperable payment networks experience faster digital transformation. These studies confirm that glocal systems are not a passing trend. They are the natural next step for global commerce and fintech growth.

A glocal payment system relies on several technical parts that work together smoothly.

A glocal payment platform acts as the core infrastructure. It includes the APIs, settlement logic, currency management, partner connections, and technical backbone that power transactions. It also enables businesses to easily plug in new local payment methods.

Glocal payment software refers to the modules built on top of the platform. These modules include dashboards, admin tools, merchant onboarding systems, reporting pages, and reconciliation panels. They help teams manage operations without touching the technical core.

A glocal payment app serves as the customer-facing layer. Users interact with this app to make payments, send money, view balances, manage wallets, or receive payouts. The app focuses on user experience, visual design, trust, and easy navigation.

The global payment landscape is changing fast. Businesses now want systems that feel global yet behave like local payment solutions. This shift fuels the demand to build glocal payment systems that can support real use cases across borders.

Local payment methods continue to rise in eCommerce. Users trust their own regional rails more than traditional cards. According to The Fintech Times, research from Boku and Juniper Research shows that over 50 percent of global eCommerce transaction value will come from non-card local payment methods by 2028. This trend underscores how important it is for companies to accept UPI, Pix, iDEAL, Alipay, and other domestic payment methods.

Central banks are speeding up work on CBDCs. These new currencies aim to make cross-border payments cheaper and faster. Cross-border real-time rails are also evolving. Businesses now want glocal systems that can support these new infrastructures from day one.

Interoperability plays a significant role in this growth. IMF research notes that digital payment adoption accelerates when systems can connect and communicate across borders. This insight supports the growing demand for glocal payment platform development and glocal payment app development for businesses that operate internationally.

India delivers a strong example of a glocal-ready environment. UPI offers instant transfers, QR payments, and wide interoperability. IMF studies highlight its role in transforming India’s payment ecosystem. The success of UPI pushes global companies to rethink how they create glocal payment systems that support local bank rails.

Brazil shows a similar story. Pix has become a national standard for real-time transfers and merchant payments. Reports from The Fintech Times confirm that Pix adoption shapes new trends in alternative payment methods. This makes Brazil a powerful example of why businesses should develop glocal payment platforms that adapt to these fast-changing rails.

Several companies are already building solutions that follow the glocal model.

These examples show why more businesses now want to build glocal payment software that matches their expansion goals. The demand is strong and growing.

Regulators and central banks shape the direction of payment innovation. Many countries introduce rules that promote real-time payments, local settlement systems, and stronger consumer protection. These changes help companies launch glocal products without facing unnecessary roadblocks.

Interoperability also receives strong policy support. IMF Fintech Notes explain how connecting domestic payment systems boosts adoption and lowers costs. These insights help businesses see why it is smarter to create glocal payment platforms that can link multiple domestic rails.

Risk and compliance remain essential. Every market follows its own laws around AML, data privacy, reporting, and fraud monitoring. Companies now prefer partners who understand local rules deeply. This underscores the need for glocal payment system development services that prioritize a compliance-first architecture.

The direction is clear. Global businesses want speed. Local users want comfort. Regulators want safety. Glocal systems meet all three needs while helping companies scale across borders.

Developing a modern glocal payment system demands a clear strategy, a strong technical foundation, and embedded compliance frameworks that support both global expansion and local market adaptation. Let’s go through a complete, streamlined roadmap every fintech leader needs when planning to build glocal payment systems.

Successful glocal payment system development starts with defining what the system must achieve.

Set Clear Objectives

Understand Local Markets

Choose the System Model

This is the core of glocal payment system development, where the blueprint turns into a scalable, secure, interoperable system.

Build a Modular, API-First Architecture

Integrate Local & Global Payment Rails

Design Settlement, FX & Ledgering

Add Risk, Fraud & Compliance Tools

Develop Dashboards, Monitoring & Reporting

Even though this is a system-level build, local user behavior must be embedded at every layer.

Localization Engine

Security & Certifications

Testing is not optional but fundamental in every glocal payment system development lifecycle.

Technical Testing

Regulatory & Compliance Checks

Once built, a glocal payment system should scale efficiently.

Phased Rollouts

Partnership-Led Scaling

Bonus Read: A Complete Guide to Fintech App Development

When you plan to build a glocal payment system, these are the major cost drivers you need to account for:

Let’s now go through the estimated cost ranges to build different layers of your glocal payment system.

| Component | Estimated Development Cost |

|---|---|

| Glocal Payment System (Core Infrastructure) | ~ US$150,000 – US$500,000+ |

| Glocal Payment Platform (API-first, modular) | US$100,000 – US$400,000+ |

| Internal / Operational Software (admin, risk, dashboards) | US$40,000 – US$150,000+ |

| Customer-Facing Payment App | US$50,000 – US$300,000+ |

Basis & justification for these ranges:

Now the question is, why such wide bands?

Because glocal payment systems are highly variable:

When you build glocal payment systems, how you price that system (internally or to clients) and how you generate ROI is critical.

Transaction-based pricing

Subscription / Platform licensing

Hybrid model

Well, when it comes to reasons, the list is large. Let’s go through the key ones.

Recommendations:

Also Read: How To Build a P2P Payment App?

It goes without saying that the global payments landscape is experiencing a seismic shift, driven by digital transformation, consumer expectations, and geopolitical realignment. Businesses and fintech innovators building glocal payment systems are positioned to leverage these trends for exponential growth and competitive advantage.

Well, when it comes to emerging trends in the glocal payment system development, the list is large. To make it short, here are the major ones that can make the difference.

1.Rise of CBDCs & Advanced Cross-Border Payment Rails – Central Bank Digital Currencies are accelerating global financial interoperability. CBDC adoption supports frictionless international settlements, enabling near-real-time cross-border payments, reduced FX complexity, and improved transparency. This all directly improves the performance of glocal payment systems.

2.Tokenization, Smart Wallets & Digital Identity Integration – Tokenization is becoming a default security architecture in real-time payments, while digital identity (e.g., eID, Aadhaar, SingPass) ensures trust, compliance, and instant KYC. The integration of smart wallets, tokenized assets, and identity-linked transactions will power next-generation cross-border flows.

3.Decentralized, Blockchain-Based Payment Overlays – Blockchain and Layer-2 networks enable ultra-low-cost, transparent, and secure payments, thus bypassing traditional correspondent banking delays. Research initiatives like SecurePay and peer-reviewed frameworks published via arXiv highlight how decentralized rails can boost interoperability and settlement assurance.

4.Inter-Ledger & Cross-Ledger Payment Infrastructure – Protocols such as Interledger, SPON, and other inter-chain frameworks enable value transfer between heterogeneous financial systems. This unlocks fully agnostic payment acceptance, regardless of currency, network, or geography, for global merchants and fintechs. Thus, fueling scalable glocal payment platforms.

5.Geopolitical Realignments Creating Alternative Financial Networks – Sanctions, global conflicts, and regional alliances are driving the emergence of new payment corridors and de-dollarization strategies. Countries are building independent SWIFT alternatives and domestic payment rails, thus increasing the need for interoperable glocal payment solutions that support multiple ecosystems.

You must not miss the latest trend in the form of Green App Development.

The global financial environment is moving toward greater fragmentation and hyperlocalization. Businesses that invest now in glocal payment system development secure a long-term competitive advantage. Here are a few reasons that prove why glocal payments are a high-ROI future Investment.

1.Rising Fragmentation in Global Payments – Local real-time rails (such as UPI, PIX, FedNow, SEPA) are growing rapidly. Apart from this, regulatory divergence is expanding region-specific compliance mandates, thereby increasing demand for unified, cross-border-friendly glocal platforms.

2.Need for Interoperability & Local Trust – Consumers trust local payment methods more than international gateways. Supporting local wallets, banking rails, and alternative payment methods (APMs) improves conversion rates, reduces cart abandonment, and enhances user confidence.

3.First-Mover Advantage and Scalable Growth – Companies building glocal payment systems today gain a strategic advantage by owning their own proprietary infrastructure rather than renting from PSPs. This leads to:

Last but not least, glocal payment systems represent the future of financial technology, blending global reach with local precision. Businesses that embrace this shift now will dominate cross-border commerce and unlock unprecedented revenue potential over the next decade.

Also Read: Build a Stock Trading App: Features, Cost, Development Process & Trends

Building a reliable, scalable, and revenue-driven glocal payment system requires deep technical expertise, mastery of payment infrastructure, and a clear understanding of global and local regulatory landscapes. That’s where Apptunix delivers unmatched value.

Apptunix has a strong track record in fintech app development, payment platform engineering, and custom payment system development. Our team understands cross-border flows, local payment rails, KYC/AML frameworks, fraud prevention models, and compliance standards. And this is almost everything needed to launch a high-performance glocal payment platform, system, or app. We bring real experience building mission-critical financial systems that demand high uptime, security, and scalability.

Every business has a unique market footprint and growth roadmap. Apptunix builds custom glocal payment systems with flexible and future-ready architectures that adapt across countries, currencies, wallets, banking rails, and regulatory environments. Don’t forget that your platform will be engineered to scale, whether you are entering two markets, twenty, or more.

Apptunix supports you across the entire lifecycle of your glocal payment system:

✔ Strategy, discovery, and technical planning

✔ UI/UX for payment flows across global and local users

✔ Core system development

✔ Compliance, KYC/AML, and risk management setup

✔ Settlement, reconciliation, and reporting

✔ Ongoing optimization, updates, and maintenance

✔ Security, compliance, speed, and performance are integrated from day one.

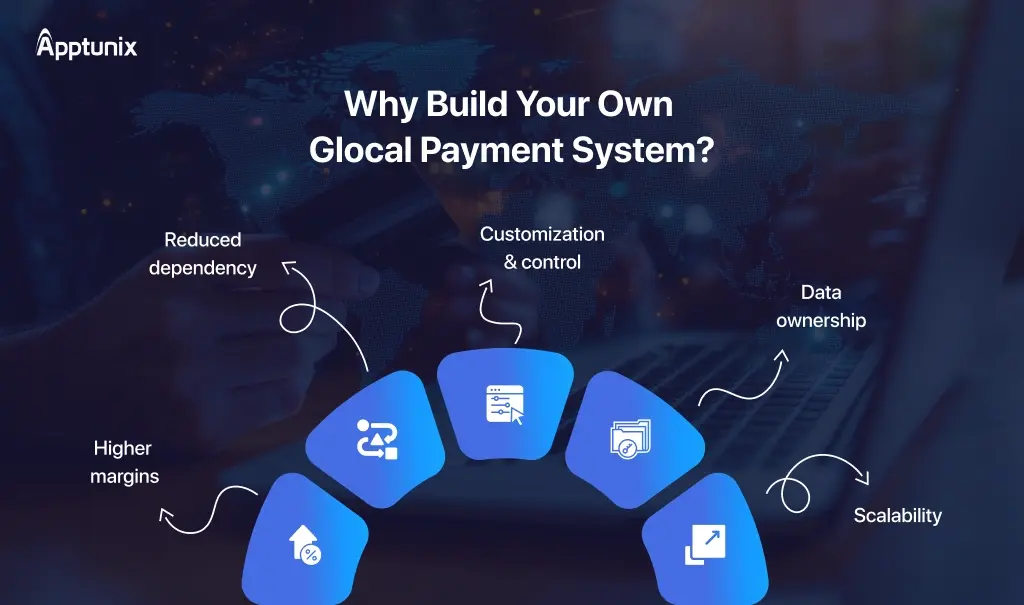

By partnering with Apptunix, you can deploy your own glocal payment system rather than rent someone else’s.

This empowers you to:

✔ Reduce dependency on third-party payment gateways

✔ Capture higher margins through your own rails, routing, and FX logic

✔ Own and control your payment data

✔ Build trust with local users in every market

Don’t miss a bonus read: Your Ultimate Guide to Create a Custom Payment Gateway

Finally, you can compete with global fintech leaders using a platform engineered exclusively for your needs

By the way, Apptunix as a leading fintech app development company also offers transparent development models, predictable cost structures, and long-term scalability, thus making your investment far more profitable than relying on generic PSPs. Then why not give it a Try?

Q 1.What is a glocal payment system?

A glocal payment system is a unified payment infrastructure that lets you accept global payments while supporting local payment methods, currencies, and regulations. It is like a smart bridge between international customers and local financial rails. This system is built through glocal payment system development practices that ensure smooth, compliant, and localized transactions.

Q 2.How much does it cost to build a glocal payment platform?

The cost to build a glocal payment platform ranges from $150,000 to $500,000+, depending on features, countries covered, local payment integrations, compliance requirements, and scaling needs. Businesses usually invest more when they need advanced capabilities like multi-currency settlement, risk engines, and local payment method integrations.

The exact glocal payment platform development cost depends on your scope, but you get a solution built for long-term revenue and not a rented PSP.

Q 3.How long does it take to develop glocal payment software or a glocal payment app?

Timelines depend on complexity. A basic version may take 3 – 6+ months, while a full-scale glocal payment software or glocal payment app with FX, routing, dashboards, and compliance modules can take 6 – 12+ months or even longer. If you are targeting multiple markets with unique local payment methods, expect a more detailed development timeline. But the end result is worth it – your business owns the entire payment flow.

Q 4.What are the main risks in glocal payment system development?

The biggest risks include compliance challenges (KYC/AML), integration issues with local payment rails, evolving regulations, fraud exposure, and data security concerns. Here, you must know that a well-planned glocal payment system development roadmap backed by compliance, security, and risk frameworks can eliminate most of these risks before launch.

Q 5.Can my business benefit from building its own glocal payment system?

Absolutely. If you are scaling across countries, building your own glocal payment system helps you reduce payment failures, own your transaction data, increase approval rates, and save big on third-party PSP fees. It also gives you full control over user experience, routing logic, and revenue from cross-border transactions.

Q 6.What features should a glocal payment platform include?

At minimum: local payment method support, multi-currency processing, FX management, fraud prevention, routing, merchant dashboards, reconciliation, and reporting. Modern glocal payment platform development also includes tokenization, real-time analytics, and API-first architecture.

Q 7.Do I need licenses to launch a glocal payment system?

Yes, depending on your markets. Many countries require payment facilitation licenses, money service business registration, or approvals from central banks. You must know that during glocal payment system development, your compliance strategy must ensure proper KYC, AML, data privacy, and local regulatory mapping.

Q 8.What technologies are used to build glocal payment software?

Developers typically use microservices, API-first architecture, secure cloud infrastructure, PCI-DSS frameworks, and integrations with local payment rails. For advanced setups, businesses can also explore blockchain, tokenization, and digital identity layers, especially in modern glocal payment software development.

Q 9.Is a glocal payment app necessary if I already have a platform?

A glocal payment app isn’t mandatory, but it gives you additional reach and convenience, especially if your customers are mobile-first. It helps you deliver localized payment experiences with local methods, currencies, and checkout flows. Many businesses choose to build both for maximum adoption.

Q 10.Why should I choose custom glocal payment system development instead of off-the-shelf solutions?

Because custom development gives you ownership, flexibility, and control. You are not stuck with PSP limitations, foreign approvals, high fees, or poor success rates. With a custom glocal payment system, platform, software, or app development, you control the entire stack. This way, you can reduce dependency, improve margins, and build a long-term competitive advantage.

Get the weekly updates on the newest brand stories, business models and technology right in your inbox.

Hardeep Singh is a seasoned B2B technical writer at Apptunix with a sharp eye for strategy and a mind wired for innovation. With over a decade of experience in technical and SEO writing, and a Master’s degree in Wireless Communication, he’s written across domains including AI, Blockchain, IoT, Cybersecurity, and beyond. At Apptunix, Hardeep drives content that bridges business goals with future-ready mobile and web solutions, thus helping startups and enterprises make smarter digital decisions.

Book your consultation with us.

Book your consultation with us.

One Central, The offices 3, Level 3, DWTC, Sheikh Zayed Road, Dubai

+971 50 782 1690

Offer Ends Soon

Get a quick expert response in under 5 minutes.