Airbnb Business Model & Revenue Strategy: 5 Insights for New-Age Businesses

6718 Views 9 min January 8, 2026

With over 20+ years of experience in driving global digital initiatives, Nikhil Bansal is the CEO & Director of Apptunix. He specializes in orchestrating large-scale digital transformations, enterprise-grade software solutions, and high-level business strategies that redefine industry standards. Nikhil is known for his ability to bridge the gap between complex business challenges and innovative technology, helping Fortune 500 companies and startups alike achieve sustainable growth. A visionary leader, he empowers enterprises to navigate the digital landscape with agile, ROI-focused models and future-ready business strategies.

Want to make a big purchase, but paying the full amount at once – that makes us think twice, right?

What about “Pay at your own pace!” – sounds intriguing, doesn’t it? Well, that’s exactly what Affirm, one of the major BNPL (Buy Now, Pay Later) services, is all about.

It’s not your typical credit card alternative; instead, it offers much more than that. Affirm empowers customers to split their payments into manageable amounts – without any hidden fees, compounding interest, or penalty. With a few taps, you can checkout with confidence, choose how and when you want to pay, and stay transparent about your costs. And for businesses? It means higher conversion, bigger orders, and happier customers.

In today’s guide, we’ll thoroughly explore Affirm’s business model and revenue model, SWOT analysis, and much more—time to see what makes it tick.

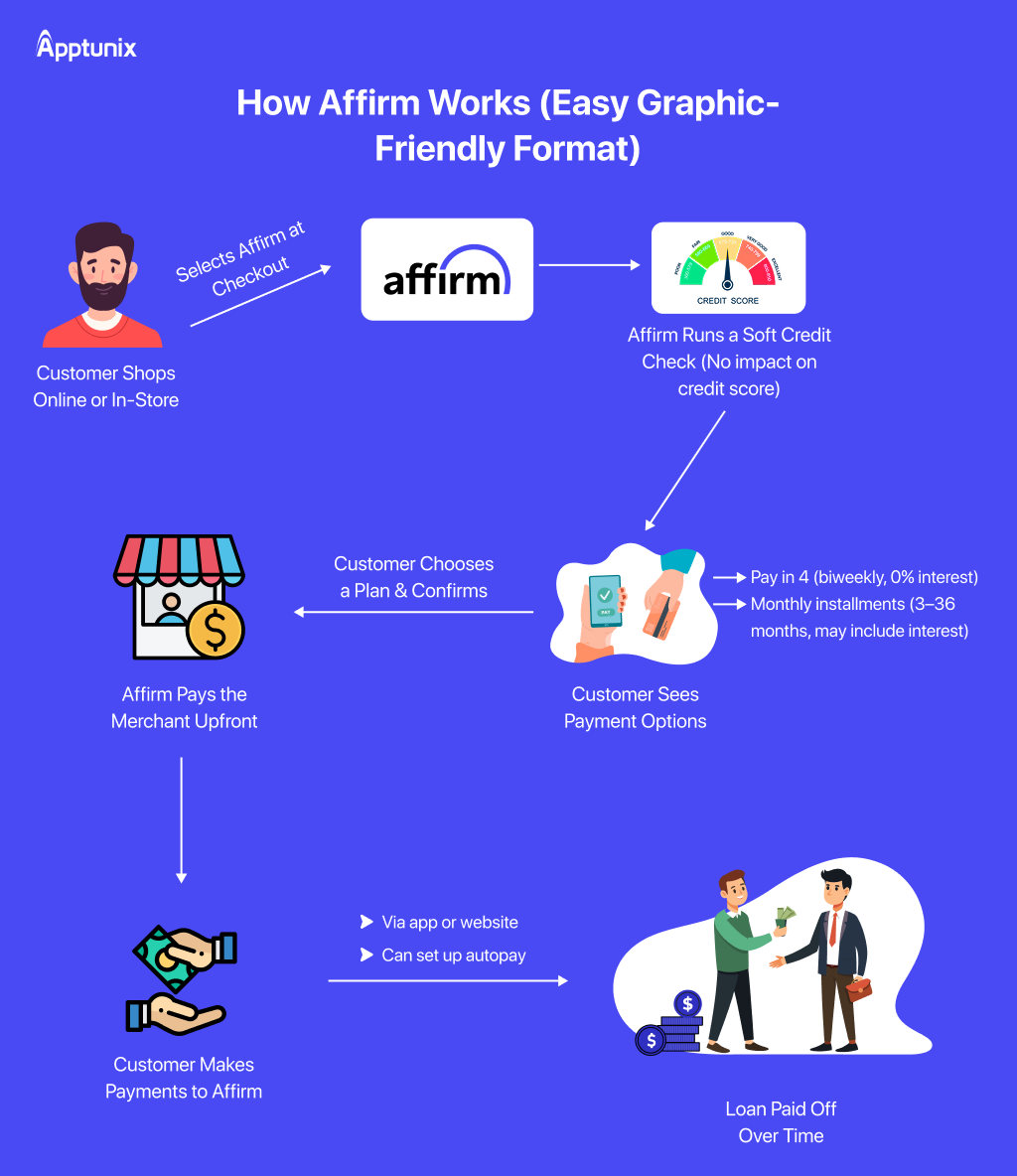

You must’ve seen the “Pay in 4 with Affirm” button when checking out on Amazon or Walmart and wondered what it means? That’s your perfect alternative: buy now, pay later (BNPL), which allows you to split your purchase into smaller, more manageable payments.

Let’s break down how Affirm works:

Affirm is a FinTech company that offers Point-of-Sale (POS) loans directly via its partner merchants, both online and in-store.

At checkout, when you choose the Affirm option, it offers to pay over time – either in 4 biweekly interest-free payments or through monthly instalments ranging from 3 to 36 months.

Affirm assesses the customer’s eligibility and the terms before finalizing the loan. Affirm evaluates the customer’s application, checking relevant information such as the FICO score. Once approved, you’ll see your details upfront, including any applicable interest rates, total cost, and exact monthly payments (without any hidden fees or charges).

Affirm then pays the retailer or merchant on your behalf, and you pay Affirm back directly through their website or app. Additionally, there are typically no late fees or penalties for early repayment, and you have the option to set up autopay or make manual payments.

However, it’s crucial to remember your due dates because Affirm might notify the credit bureaus if you do miss a payment. This makes Affirm a transparent, flexible BNPL alternative to traditional credit cards – a win-win situation for all parties involved.

Check the following facts and statistics regarding Affirm. Let’s check:

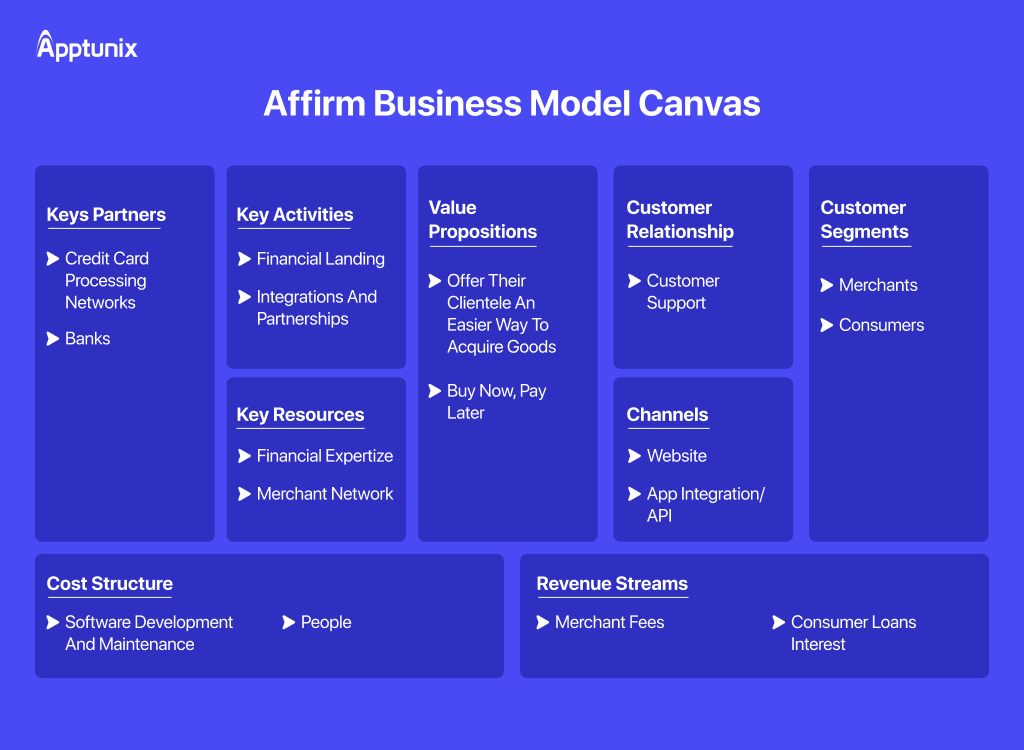

Let’s understand the business model canvas of Affirm and how it has completely transformed the BNPL market with effective fintech solutions:

1. Customer Segments2. Value Propositions3. Channels4. Customer Relationships5. Revenue Streams6. Key Activities7. Key Resources8. Cost Structure9. Key PartnershipsLet’s take a look at how Affirm makes money with its BNPL service solutions:

1. Interest Income from ConsumersAffirm generates revenue by charging interest on the loans it offers. Certain loans provide zero-interest financing, while others have an annual percentage rate (APR) of up to 30%, depending on the credit history of the borrower. The average loan size is $750, but it may reach $17,500, and about 43% of loans are interest-free.

Although they don’t charge late or hidden fees, interest accounts for a sizable amount of their revenue.

2. Merchant Fees (Affirm’s Core Revenue Stream)A processing fee, often ranging from 2 to 6% of each transaction, is assessed to merchants by Affirm. Why do merchants agree? Affirm benefits both parties by increasing average order value, reducing cart abandonment, and boosting revenues.

Note: Affirm either underwrites directly through Affirm Loan Services or collaborates with banks like Celtic Bank and Cross River Bank to fund some loans. This enables them to grow rapidly without taking on significant capital risk.

3. Virtual Card TransactionsLike credit card issuers, Affirm makes money by serving as the issuer and collecting fees from transactions made by users using its virtual cards to shop at non-partner merchants.

4. Late Payment Reporting (Not Fee-Based)Although Affirm doesn’t impose late fees like traditional lenders do, it does notify credit bureaus of late payments, which serves more as a means of encouraging credit behavior than a revenue stream.

5. Strategic Partnerships & Platform IntegrationsAffirm earns from partnerships with eCommerce platforms (like Shopify and Amazon). It becomes the preferred BNPL option on these eCommerce platforms —leading to more transactions and broader market reach.

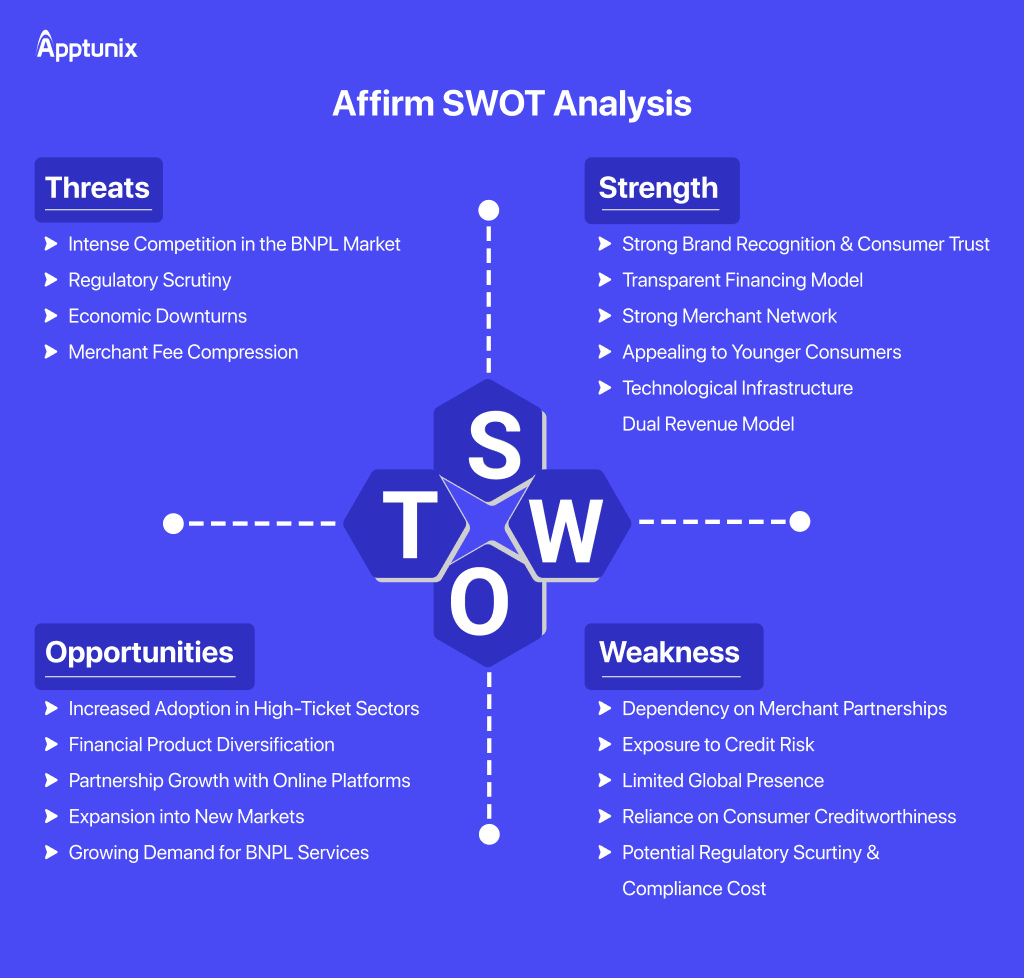

Following, we’ve discussed the SWOT (Strengths, Weaknesses, Opportunities, Threats) analysis of the Affirm business strategy model. Let’s learn:

1. StrengthLet’s take a look at the strength aspect of Affirm’s business & Affirm’s revenue model:

2. WeaknessLet’s take a look at the weakness aspect of the Affirm business & revenue model:

3. OpportunitiesLet’s take a look at the opportunities aspect of the Affirm business & Affirm revenue model:

4. ThreatsLet’s take a look at the threat aspect of the Affirm buy now and pay later model:

Let’s take a look at how Affirm payment plans work:

| Feature | Pay in 4 | Monthly Installments |

|---|---|---|

| Purchase Amount | $50–$1,000+ | $50–$5,000+ |

| Payments | 4 total | 3 to 60 months |

| Schedule | Every 2 weeks | Monthly |

| Down Payment | May be required | May be required |

| Interest | Interest-free | 0–36% APR |

| Fees | None | None |

| Credit Impact (Apply) | No impact | No impact |

| Credit Impact (Loan) | May impact if accepted/due | May impact if accepted/due |

Affirm is transforming the way people pay – it’s reshaping the psychology of purchasing. It’s paving its way to eliminate friction that often stops consumers mid-checkout.

In today’s Buy Now and Pay Later revolution, Affirm is standing firm in this ecosystem. By offering flexible, transparent, and interest-free (in some cases) financing options, Affirm is becoming a top priority for consumers. Here’s the most impressive catch: Affirm monetization strategy without traditional fees, making it a win-win solution for both customers and merchants. If you’re eyeing a similar BNPL business model like Affirm in this competitive FinTech industry, get in touch with our experts.

If you’re ready to enter the booming Buy Now, Pay Later (BNPL) market and build a BNPL app like Affirm, choosing the right development partner is critical to your success.

Apptunix, a leading name in FinTech app development, is here to help you turn your BNPL vision into a powerful, scalable reality.

In a competitive financial landscape, you can’t afford to settle for a basic product. So, you need a solution that’s not only technically sound but also user-centric, compliant, and future-ready.

At Apptunix, we blend cutting-edge technologies with FinTech expertise to build apps that can outperform and scale seamlessly. When you work with us, you get:

Whether you want to create a flexible payment model, a virtual card system, or integrate with eCommerce giants like Shopify or Amazon, we’ll build the infrastructure you need to thrive in the BNPL space.

Q 1.What is the business model of Affirm?

Affirm operates on a Buy Now, Pay Later (BNPL) business model. It partners with merchants to offer customers point-of-sale financing options and earns revenue from interest on loans and merchant fees.

Q 2.What kind of business is Affirm?

Affirm is a financial technology (fintech) company that offers consumer lending services. It enables shoppers to split purchases into monthly installment payments, often at 0% APR, directly at checkout.

Q 3.How much does it cost to build a BNPL app like Affirm?

The BNPL app development cost typically costs between $20,000 and $300,000+, depending on features, integrations, and platform complexity.

Q 4.How long does it take to develop a BNPL app like Affirm?

BNPL app development like Affirm takes around 3 to 9 months, based on the project’s complexity, features, design, and more.

Q 5.How does Affirm make money at 0%?

Affirm earns money at 0% APR loans by charging the merchant a higher processing fee. Merchants cover the interest costs in exchange for increased conversions, higher order values, and improved customer retention.

Q 6.What is the revenue model of Affirm?

Affirm’s revenue model includes:

Q 7.How does Affirm earn revenue?

Affirm earns revenue through a mix of:

Q 8.Will Affirm impact my credit score?

Affirm may or may not impact your credit score. For 0% or short-term loans, they often use a soft credit check, which doesn’t affect your score. But for longer-term loans, they may report to credit bureaus, which can affect your credit history.

Q 9.What is the business breakdown of Affirm?

Affirm’s revenue primarily comes from:

Q 10.Is Affirm safe to use?

Yes, Affirm is considered safe and uses bank-level encryption. It also discloses terms clearly, with no hidden fees or compounding interest.

Q 11.Who are Affirm’s main competitors?

Affirm competes with other BNPL companies like Afterpay, Klarna, Splitit, PayPal Credit, Perpay, and Zip, as well as traditional credit card providers and banks offering installment loans.

Q 12.Does Affirm check your credit?

Affirm, an online financing platform uses soft credit checks for most loans, but hard inquiries may be performed for longer-term, which can affect your credit score.

Q 13.Can I pay off my Affirm loan early?

Yes, Affirm allows early repayment at no extra charge. Paying early can help reduce the total interest paid on non-zero APR loans.

Q 14.What factors does Affirm consider before approving a loan?

Affirm uses a proprietary algorithm to decide who qualifies for a loan and on what terms. It considers:

This smart system ensures most borrowers repay their loans on time, keeping risk low and revenue steady.

Q 15.When did Affirm launch its consumer app?

Affirm launched its consumer app in October 2017, allowing users to access loans for purchases at virtually any retailer. This app significantly expanded Affirm’s reach and made “buy now, pay later” options more accessible to everyday shoppers.

Q 16.Is Affirm available at Walmart?

Yes, Affirm partnered with Walmart. This partnership enables Walmart customers to use Affirm both in-store and online to finance their purchases. It’s a major collaboration that brought BNPL to one of the largest retail chains in the world.

Q 17.Which eCommerce platforms support Affirm?

Affirm is integrated with several major eCommerce platforms, including:

These partnerships allow online merchants using these platforms to offer Affirm as a payment option at checkout easily.

Q 18.Is Affirm partnered with Amazon?

Yes, Affirm became Amazon’s exclusive BNPL partner in the U.S. This allowed eligible Amazon shoppers to split purchases into monthly payments, directly leveraging Affirm’s financing model within the Amazon shopping experience.

Q 19.Can I use Affirm at any retailer?

Yes, users can apply for loans and shop at nearly any retailer. The app generates virtual cards for use wherever Affirm is accepted, greatly increasing flexibility for consumers.

Get the weekly updates on the newest brand stories, business models and technology right in your inbox.

With over 20+ years of experience in driving global digital initiatives, Nikhil Bansal is the CEO & Director of Apptunix. He specializes in orchestrating large-scale digital transformations, enterprise-grade software solutions, and high-level business strategies that redefine industry standards. Nikhil is known for his ability to bridge the gap between complex business challenges and innovative technology, helping Fortune 500 companies and startups alike achieve sustainable growth. A visionary leader, he empowers enterprises to navigate the digital landscape with agile, ROI-focused models and future-ready business strategies.

6718 Views 9 min January 8, 2026

6893 Views 9 min December 21, 2025

7517 Views 9 min November 26, 2025

Book your consultation with us.

Book your consultation with us.

One Central, The offices 3, Level 3, DWTC, Sheikh Zayed Road, Dubai

+971 50 782 1690