Fleet Management Software Development: Cost, Features, Process & AI Guide for Enterprise Fleets

90 Views 10 min June 24, 2026

Pallavi Nautiyal is a seasoned Tech Consultant at Apptunix, specializing in the intersection of global finance and decentralized technology. With a deep-rooted expertise in banking infrastructure, digital payment gateways, and Web3 ecosystems, she guides businesses through the complexities of modern financial engineering. Pallavi is recognized for her ability to architect secure, compliant, and scalable solutions—ranging from smart contracts and crypto-wallets to robust digital banking platforms. Her strategic insights help organizations navigate regulatory landscapes while leveraging the power of Blockchain to ensure transparency and seamless user experiences in every transaction.

A few years ago, Allstate was facing a problem most legacy insurers won’t admit publicly. With customer expectations changing, they were slowly becoming irrelevant. People wanted instant quotes, faster claims, and seamless digital experiences. But behind the scenes? Their systems were still doing things the old way. Fragmented data, slow updates, and processes that weren’t built for real-time anything.

So, they made a shift to the cloud, not just to modernize IT, but to rethink how the business runs. Faster claims, real-time data, and quicker product launches followed.

Allstate’s move wasn’t an isolated case. Across the industry, insurers are investing heavily in the cloud to stay competitive and meet modern customer expectations. In fact, the global cloud computing in the insurance market is projected to grow to approximately USD 40.76 billion from USD 15.23 billion by 2034, expanding at a compound annual growth rate (CAGR) of around 11.56%. This shows just how big this shift has become.

So, here’s the question for founders:

If a legacy giant had to reinvent itself to stay competitive, what does that mean for startups today?

Because this shift isn’t just about big insurers.

It’s about the rise of cloud-based insurance solutions and a massive gap waiting to be filled by founders who understand where the industry is headed.

And that’s exactly what we’re going to break down in this blog.

Cloud computing in insurance isn’t just moving servers to someone else’s data center. It’s the shift from capex‑heavy and slow IT to scalable and connected technology stacks that evolve with markets and regulations.

At its core, cloud computing in the insurance world is used to:

This shift enables insurers to innovate faster, make data‑driven decisions, and embrace digital transformation.

While cloud computing clearly redefines how insurers operate at a technical level, the real question is: why has it become so critical for the industry right now?

Insurance has lasted for over a century by minimizing risk, which makes it inherently risk‑averse.

Legacy systems in insurance are often decades old, disjointed, and expensive to maintain. They were never designed for the digital age, real‑time mobile experiences, IoT data integration, or even for AI‑driven insights.

The benefits of cloud computing in insurance for insurers:

While the need for cloud solutions in insurance is clear, what’s even more compelling is how rapidly the industry has already begun adopting them at scale.

Cloud adoption in the insurance industry has reached high levels. Over 85% of insurers are expected to run critical workloads on cloud platforms by the end of this year.

This surge in adoption numbers happened because of pressure, not just from competition but from customers as well. Today’s policyholders expect:

All of which rely on agile, data‑driven systems that only cloud computing can deliver at scale. This is how cloud computing makes a real difference in insurance, which we can see in its key use cases.

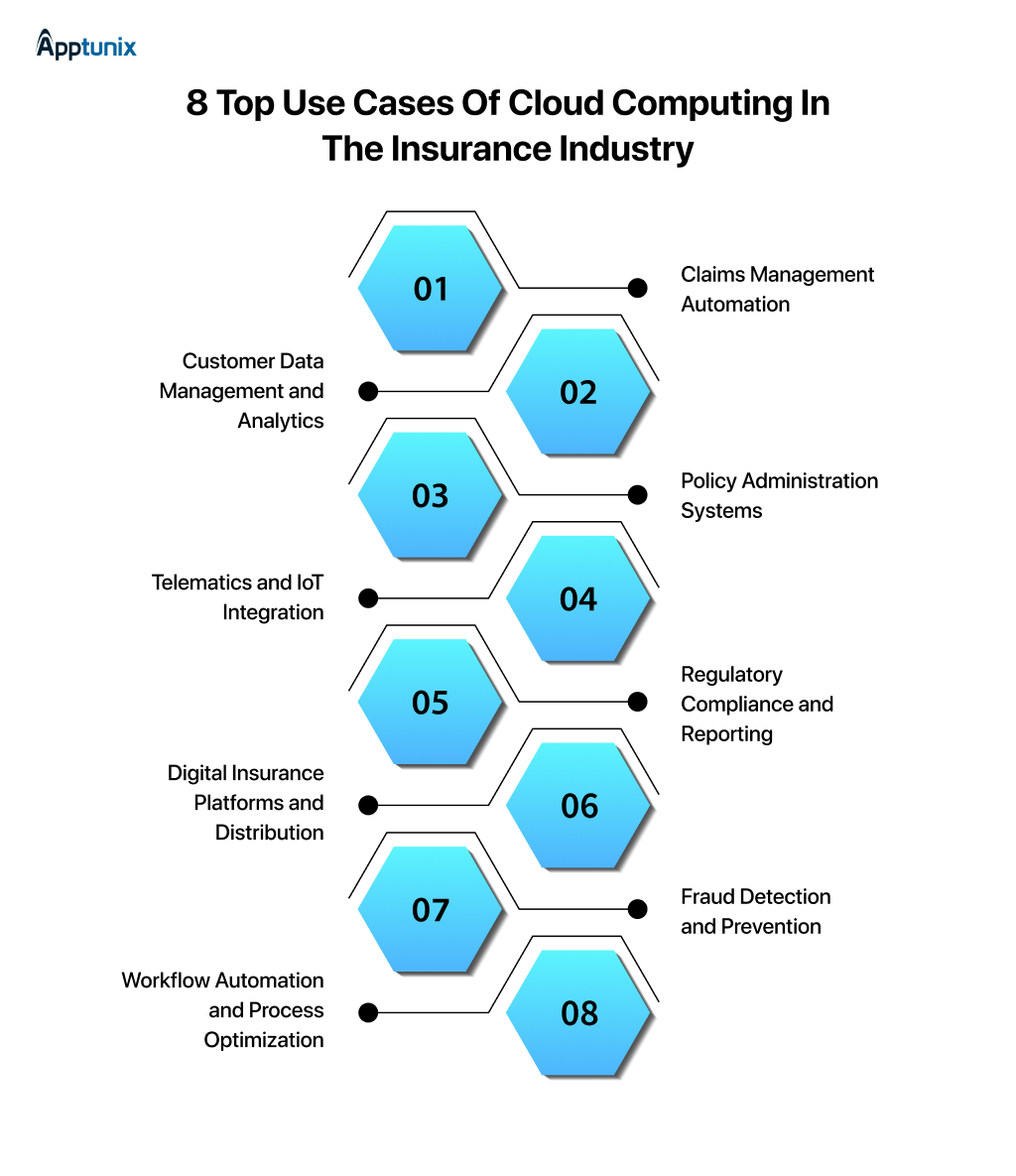

Here’s where we talk about the high‑impact use cases where cloud computing is changing how insurance works:

1: Claims Management AutomationClaims are the heart of insurance operations and the part customers hate the most. Traditional processes are manual and slow, with high error rates. Cloud computing enables:

Startups can offer insurance software cloud solutions that can significantly reduce claim processing times. This will, in turn, free up the staff for more complex cases and improve customer satisfaction as well.

2: Customer Data Management and AnalyticsInsurance companies collect massive amounts of customer data: demographics, claims history, risk profiles, preferences, payments, you name it.

Without the cloud, that data lives in silos, making it inaccessible, unanalyzed, and underused. Cloud computing enables:

Imagine a platform where an insurer can answer questions like:

That’s the power of AI-powered cloud insurance solutions. To stand out in the market, you can also incorporate an analytics layer or AI assistants that help insurers turn raw data into decisions quickly.

3: Policy Administration SystemsPolicy admin systems are the engines that power quotes, renewals, underwriting, and billing. Traditionally, these are rigid systems that require weeks, sometimes even months, to update.

But with cloud‑native systems:

Cloud solutions help insurers cut product launch times from weeks to mere hours in some cases. This is the real potential of the cloud for the insurance industry.

4: Telematics and IoT IntegrationConnected devices like telematics in cars, wearables, and smart home sensors produce streams of data into systems that need to scale. Cloud powers real‑time ingestion and analytics so insurers can:

Cloud, when combined with IoT, is a new product category. It offers usage-based and on-demand insurance that literally pays customers based on how they behave. In the coming time, platforms that normalise and score IoT data will be strategic assets.

5: Regulatory Compliance and ReportingInsurance is one of the most regulated industries in the world. Compliance isn’t optional. And regulators demand transparency, audit trails, and security.

Cloud platforms offer:

In other words, cloud computing in insurance isn’t just operationally valuable; it’s also compliance‑enabling.

6: Digital Insurance Platforms and DistributionCustomers don’t want to call agents anymore. They prefer instant quotes on apps, personalized bundles, and 24/7 service. Scalable cloud-based insurance platforms form the backbone of modern distribution. Cloud-native digital platforms make this possible through:

Digital distribution is only possible with scalable cloud platforms at the core. If you’re building cloud-based on-demand insurance apps, this is one of the most tangible, revenue‑generating areas to target.

7: Fraud Detection and PreventionInsurance fraud is still very prevalent, and companies lose billions because of that. Cloud platforms allow insurers to:

With the help of consolidated cloud data lakes and machine learning models, insurers are catching fraud patterns earlier and more accurately than ever.

For founders, this is a huge opportunity to integrate plug‑in analytics and AI fraud engines that sit on top of cloud data architecture.

8: Workflow Automation and Process OptimizationInsurance workflows traditionally involve a lot of repetitive human tasks like manual approvals, email chains, and more.

Cloud systems can orchestrate workflows across teams using tools like low-code automation, serverless functions, and real-time tracking, particularly when built on cloud engineering in agile principles.

Findings show workflow automation can cut processing time by 30-50% in core insurance functions like policy issuance and claims.

Okay, let’s pause for a reality check. Cloud is powerful, but it’s not magic. There are real obstacles you need to understand.

1: Data Security and Privacy ConcernsInsurance data is highly sensitive information. All the policyholder details, health info, and financials are regulated by laws like GDPR, HIPAA, and other privacy laws.

Now, we are not saying that cloud is insecure, but there are a few things one must tackle when building cloud-based insurance solutions:

Security is not just a product layer. It’s a market requirement these days.

2: Integration with Legacy SystemsMost insurers aren’t throwing out their core systems overnight. That means your solution must bridge the gap between cloud-native and on-premise.

Your SaaS product must integrate with:

This means building flexible connectors, ETL pipelines, and hybrid architectures. Integration is where many startup projects hit the wall. But it’s also where most enterprise deals are won.

3: Regulatory and Compliance HurdlesYes, we have already mentioned this above in use cases. But from a risk perspective, we need to talk about it again. Regulators worry about data residency, solvency rules, audit retention, and consumer protections. Every cloud solution must be designed with compliance built in.

4: Skill and Knowledge GapsInsurers have talented people, but many don’t have cloud‑native experience. This creates:

Founders must be educators, not just sellers. If you can enable and educate, that’s a value add.

5: Cost Management and FinOpsCloud saves money only if you control usage. Unmanaged instances, data egress charges, and idle compute waste budgets fast.

Founders must build with FinOps in mind:

This is a differentiator for wise SaaS founders.

The impact of these applications is just the beginning. Cloud is setting the stage for the next wave of innovations in insurance.

Let’s look ahead, what’s next, and where your startup might win:

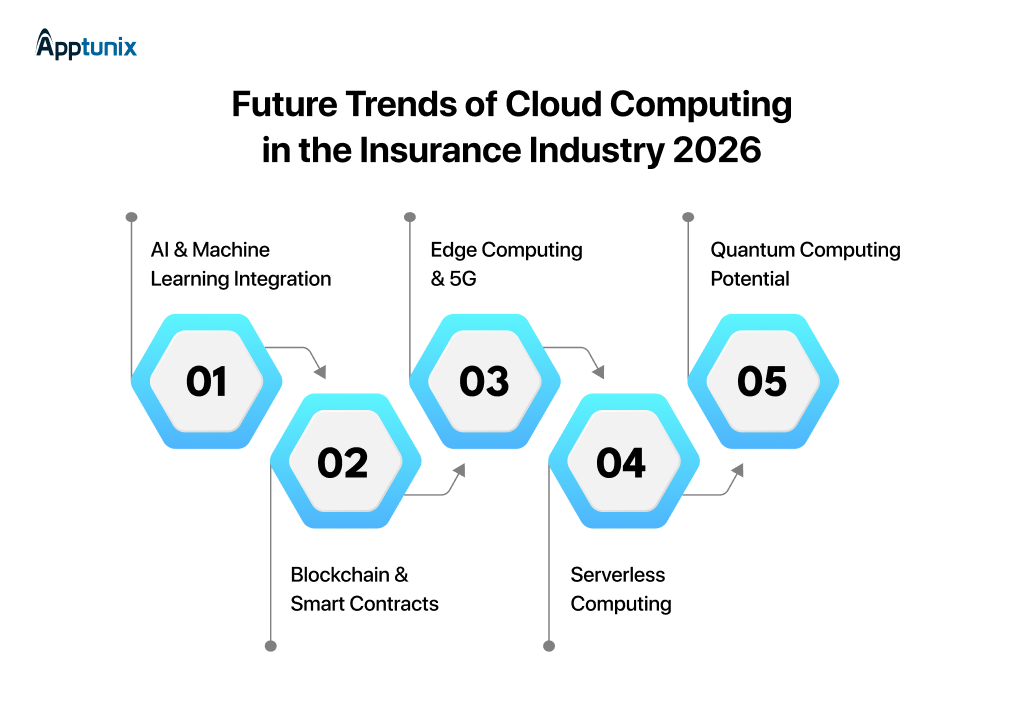

1: AI and Machine Learning IntegrationAI is reaching a point where it’s not experimental, it’s expected. Cloud makes AI usable. Insurers adopting AI for underwriting and risk scoring are seeing underwriting time cut from weeks to hours with improved accuracy.

Some examples include:

Carriers won’t buy cloud, but they’ll buy AI-powered cloud insurance solutions built on top of cloud. And that’s exactly where the real value stack lives.

2: Blockchain and Smart ContractsBlockchain pilots in claims have reduced disputes and settlement times in test environments. Smart contracts enable:

Imagine a situation where a travel insurer automatically pays out a flight delay claim without human intervention.

That’s the power of cloud and blockchain. Founders who build modular, API‑first smart contract layers stand to disrupt incumbents.

3: Edge Computing and 5GWith edge computing and 5G, real-time data from vehicles and devices can be processed closer to the source. This means:

4: Serverless ComputingFor startups in insurance, serverless means:

If you’re building APIs or ML scoring engines, serverless makes your product cheaper and faster.

5: Quantum Computing PotentialStill experimental, but quantum computing could change risk modeling and optimization problems. It could help with:

This isn’t immediate, but top cloud service providers are already exploring quantum services. Insurers who experiment early will gain a competitive edge. With these opportunities in mind, let’s look at how SaaS founders can successfully sell their solutions to insurance companies.

If you’re a founder pitching cloud to an insurer, here’s what to tell them:

1: Align With Business OutcomesInsurers care about:

Cloud is the enabler, but the outcome is what matters. Show the tangible impact your product can deliver.

2: Solve One Pain Point Really WellNo insurer is going to replace their entire system overnight. Focus on a modular, cloud-based insurance solution that:

It’s better to start small and have a single USP. By doing this, they’ll be more open to scaling up.

3: Build for Compliance & Risk FirstInsurance is all about trust. You can not just claim that your platform is secure. It is very important to prove it as well:

If you handle compliance, you remove a major blocker before the sales process even begins.

4: Educate Before You SellMany insurance teams still don’t fully grasp what cloud services for insurance can do. That’s an opportunity to educate them:

Present yourself as a trusted advisor, not just a vendor who is there to sell.

5: Make Integration EasyBeing AWS‑only is limiting. Support Azure, GCP, and on‑premise hybrids to match real insurance environments. Offer APIs and pre-built connectors. Make deployment as painless as possible. The easier you fit into their workflow, the faster your product gets traction.

The potential of cloud for the insurance industry is enormous. As Allstate showed, moving to the cloud isn’t just modernizing IT; it’s reinventing how insurance businesses operate, from claims processing to real-time analytics and digital experiences.

At Apptunix, we see this as a massive opportunity for founders. Insurers are looking for cloud-based solutions that integrate with legacy systems, improve efficiency, and deliver measurable outcomes. Whether it’s AI-powered claims automation, predictive analytics, or on-demand insurance apps, the gap in the market is clear. And it’s waiting for innovators to fill it.

With experience delivering over 2,000 digital products and building AI-powered, cloud-native platforms, we help founders turn ideas into market-ready solutions. As a leading mobile app development company, we design systems that integrate with existing infrastructure, scale seamlessly, and deliver real impact.

The insurance industry is evolving fast. Are you ready to build the solutions that will define its future? Start your cloud insurance journey with Apptunix today!

Q 1.What is cloud computing in insurance?

Cloud computing in insurance refers to the use of remote servers and internet-based platforms to host, manage, and process data essential to insurance operations. It enables scalability, real-time analytics, cost reduction, and faster digital service delivery compared to traditional on-prem infrastructure.

Q 2.How does the cloud improve insurance operations?

Cloud solutions automate core processes such as policy administration, claims processing, and servicing workflows. This includes enabling digital transformation, such as using AI and machine learning for risk assessment and a better customer experience.

Q 3.What are the common challenges with cloud adoption?

Common challenges include:

Q 4.What types of cloud options are available for insurers?

Insurers can generally choose between public, private, and hybrid cloud options based on their security needs and existing IT infrastructure. These options support different deployment models, including Infrastructure as a Service (IaaS), Platform as a Service (PaaS), and Software as a Service (SaaS).

Q 5.Can cloud computing help insurers fight fraud?

Yes, cloud computing can help insurers fight fraud by enabling real-time scoring, cross-system data correlation, machine learning models, and automated alerts. Cloud data lakes provide the scale and compute required for effective fraud detection.

Q 6.How should SaaS founders price cloud insurance solutions?

Insurance buyers expect pricing tied to value delivered. Common models include:

Pricing strategy affects adoption, especially in enterprise procurement.

Get the weekly updates on the newest brand stories, business models and technology right in your inbox.

Pallavi Nautiyal is a seasoned Tech Consultant at Apptunix, specializing in the intersection of global finance and decentralized technology. With a deep-rooted expertise in banking infrastructure, digital payment gateways, and Web3 ecosystems, she guides businesses through the complexities of modern financial engineering. Pallavi is recognized for her ability to architect secure, compliant, and scalable solutions—ranging from smart contracts and crypto-wallets to robust digital banking platforms. Her strategic insights help organizations navigate regulatory landscapes while leveraging the power of Blockchain to ensure transparency and seamless user experiences in every transaction.

90 Views 10 min June 24, 2026

95 Views 10 min June 22, 2026

105 Views 10 min June 19, 2026

Book your consultation with us.

Book your consultation with us.

One Central, The offices 3, Level 3, DWTC, Sheikh Zayed Road, Dubai

+971 50 782 1690

Offer Ends Soon

Get a quick expert response in under 5 minutes.